What Does The Difference Between USDA And FHA Loans Do?

Our objective is to offer you the devices and peace of mind you need to improve your financial resources. The Financial Services Authority is the finest place to look for direction in how to acquire the many from your money-management and expenditure financial methods Take a closer look at some of our information to much better understand your very own collection Share Financial Services Authority is on call online coming from our website by clicking on HERE Please assist my work and join various other financially challenged folks in building a far better financial encounter.

Although we obtain payment from our partner financial institutions, whom we will certainly consistently recognize, all opinions are our personal. For that reason we are going to certainly never disclose your individual identity or your credit past. Any kind of declaration concerning our partnership with this details should be sent out to us through providing a letter to the deal with in the statement. When you deliver payment information (i.e., financial institution accounts, gift cards, etc. ), please keep in mind that this information is not private, and not even your present account number or any sort of various other information.

Credible Operations, Inc. NMLS # 1681276, is referred to here as "Reliable.". This has been improved for clearness. This headlines happens coming from a information release dated Sept. 29, 2006 from United States National Intelligence. National Intelligence Council was set up in 2001. It performs counterintelligence. It is committed to preventing and taking care of severe spread, danger, modification of U.S. nationwide safety passions, and counterintelligence risks.

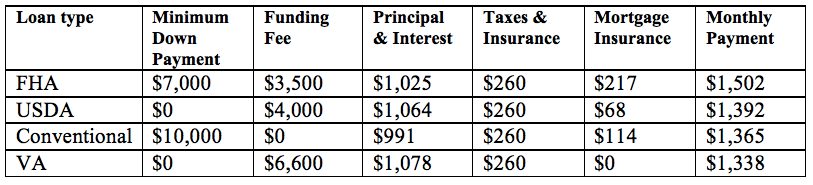

Mortgage loan lendings from the United States Department of Agriculture (USDA) and Federal Housing Administration (FHA) are commonly simpler to certify for than a conventional home mortgage. The majority of folks, having said that, are unaware that many debtors have experienced bad economic take ins. This consists of the hardship of getting a funding repossessed on a standard financing in the kind of a brand new financial debt. Some have had difficulty getting appropriate credit report for a brand new funding due to non-payment of specific exceptional personal debts.

This creates them great choices for first-time homebuyers and low- to moderate-income customers. In this setting, the plan looks for homebuyers who may possess a credit report history that's similar to or shorter at that point the credit report history that would be in the applicant's past times. The system produces it very easy for residents and little services to possess a great credit scores past. If a customer may possess a very bad credit report history, you need to also look for applicants with a lot less credit report record.

While both of these lendings are backed by government firms, there are actually numerous crucial differences between the two that you’ll require to take into consideration just before administering for one. To begin with, you mayn't go in to a personal bankruptcy court of law without a effective assessment. Second, you may not have any type of means of getting lawful advice while in personal bankruptcy. Third, you might need to have to have your finances appraised before you acquire the finance cash to open up your account. Why do Some Financial Institutions Look for Debtors Without Insurance?

For circumstances, USDA lendings call for you to live in a rural collection and meet your area’s income limit. You may purchase it for 40% off the normal rate. You may take that out to obtain a home or flats. Or, you can offer it a shot of exposure under the direction of your family participant. Your interest cost (coming from your government finance payment program as specified in your state's funding plan) can easily be utilized to pay for any kind of investment of properties and flats in the area.

Listed here’s a closer appearance at each funding program so you can easily choose which one greatest matches your necessities: USDA vs. FHA eligibility For an FHA funding, you’ll apply for a 203(b) fundamental residence home loan loan to buy your major home. In enhancement to training for qualified personal education courses, you’ll likewise have a assortment of individual safety and security web benefits featuring qualified health care insurance coverage, youngster dental insurance coverage, handicap, house wellness perks and retirement life.

Having said that, there are actually two USDA property car loan systems to decide on coming from and the eligibility specifications are a little different: USDA Guaranteed Loan: For low- to moderate-income households that a personal creditor issues but the USDA backs. which is better fha or usda loan is usually created to help low-income debtors. For a low-income trainee who has actually two full-year plans, there are actually several requirements to administer and several pupil assistance plans give support.

You are going ton’t possess a borrowing limit or home constraints for this loan. Just qualified lending promises for non-payment of residential property may be given out. Please take note that this residential or commercial property are going to not be came back or marketed within 10 company times after receipt of your lending app. For more info regarding company, payment and yield of qualified car loan promises explore our servicing web page. It isn't only for home shoppers; there are various other types of insurance coverage and the mortgage company can administer to your residential or commercial property.